Here is a number worth sitting with: $800 billion.

That is the approximate annual profit the AI infrastructure industry would need to generate just to service the interest on current investment trajectories, according to IBM’s CEO Arvind Krishna, ~who put it plainly~ late last year. Not profit to grow. Not profit to return to shareholders. Profit just to cover the interest. Revenue has not come close to that level.

This is not a technology argument. It is a financial arithmetic argument. And it is the most important thing to understand about the AI economy right now.

The Bet and Who’s Making It

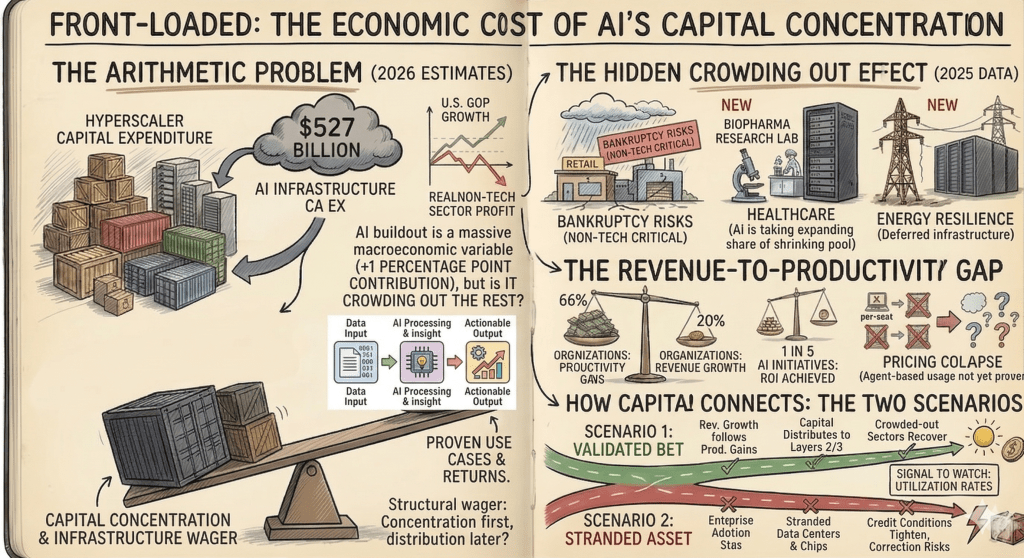

In 2026, the consensus estimates for hyperscaler capital expenditure on AI infrastructure, data centers, chips, power, and networking, is $527 billion. That figure is contributing approximately one percentage point to US GDP growth this year, making the AI buildout not just a technology investment story but a macroeconomic variable in its own right.

The capital is concentrated in a handful of companies. Three or four hyperscalers are making spending decisions so large that they individually move macro indicators. Morgan Stanley’s 2026 AI market analysis puts the AI buildout in the same tier as the peak of the telecom investment cycle in the late 1990s — a comparison worth keeping in mind.

What is being built is not just technology infrastructure. It is a structural wager: that concentrating capital in AI infrastructure before use cases are proven at scale is the right sequence. The bet is that the returns will be large enough, and arrive soon enough, to justify the scale of the commitment.

That bet may be right. It may not be. The arithmetic does not yet resolve in either direction.

The Historical Pattern

Every major infrastructure buildout in economic history has followed a version of the same sequence. Capital concentrates. Infrastructure is built ahead of demand. A period of dislocation follows. And then, if the underlying technology proves genuinely useful, returns eventually materialize and value begins to distribute more broadly.

The railroad expansion of the 1870s followed this pattern. Massive capital concentration, genuine long-term value creation, and a significant financial crisis in between. The telecommunications boom of the late 1990s followed it too: overbuilt fiber, spectacular failures, and then, a decade later, the internet economy that the infrastructure eventually enabled.

The historical pattern does not tell us that AI will crash. It tells us two things worth knowing: infrastructure overbuild before demand materializes is normal for general-purpose technologies, and the period between concentration and distribution is where economic costs tend to land. We appear to be in that period now.

What makes the current moment worth watching carefully is the scale. At $527 billion in 2026 alone, this buildout is larger relative to the broader economy than either the railroad or telecom equivalents at their peaks. The potential upside is correspondingly larger. So is the potential downside.

The Hidden Cost: What Isn’t Getting Funded

The headline capex numbers get the attention. The crowding-out effect is getting far less than it deserves.

As financial institutions concentrate lending on AI infrastructure, affordable capital is becoming scarcer for businesses outside the AI complex. In 2025, a rising number of non-tech firms were forced into bankruptcy, citing tightening credit conditions and rising input costs as primary drivers. AI capex, in other words, is masking economic weakness in the broader economy while simultaneously contributing to it.

The sectoral consequences are sharper than the aggregate numbers suggest.

In healthcare, AI investments accounted for 46% of total healthcare investment in 2025, according to Silicon Valley Bank’s annual healthcare report. That sounds like healthcare is thriving on AI investment. The fuller picture: overall healthcare investment declined 12% year over year. Biopharma investment fell 19%. Diagnostics and tools fell 33%. AI is taking an expanding share of a shrinking pool. The research pipelines, clinical tools, and healthcare infrastructure that depend on that broader pool are being quietly starved.

In energy resilience, more than $3 trillion is invested annually in energy systems, according to research published in Nature Energy, but the share allocated to resilience, hardening grids, improving storage, building redundancy remains critically inadequate. As capital gravitates toward AI data center power demand, the long-term resilience investment that aging infrastructure require is being deferred.

The long-term cost of this deferral is not abstract. Infrastructure underinvestment compounds. Healthcare research pipelines that don’t get funded in 2025 and 2026 produce gaps in treatments and tools a decade from now. Climate resilience that isn’t built today becomes emergency response cost tomorrow. The opportunity cost of AI capital concentration is not just “other technology didn’t get funded.” It is “other urgent problems didn’t get addressed during a window when addressing them was still relatively cheap.”

This is the part of the capital restructuring that extends well beyond AI economics. Capital allocation decisions made in the next two to three years will shape the structural capacity of economies in sectors that have nothing to do with artificial intelligence but everything to do with human welfare and long-term productivity.

The Revenue Problem

Back to the arithmetic. The infrastructure bet is front-loaded. The revenue assumptions are back-loaded. The gap between them is large and not yet narrowing in the way the investment scale would require.

Deloitte’s 2026 research finds that 66% of organizations report productivity gains from AI, but only 20% report revenue growth. That gap is not just a productivity story. It is a capital allocation story. Productivity gains that don’t translate to revenue don’t generate the returns that justify the infrastructure investment upstream. The money went in before the use case was proven at scale, and the use case is still being proven.

Gartner finds that only 1 in 5 AI initiatives achieves measurable ROI. Despite this, 85% of organizations increased their AI investment in the past year, and 91% plan to increase it again. Capital keeps flowing toward infrastructure whose returns remain unproven. That is the definition of a bet, not a return.

How Capital Connects to the Other Three Clocks

The capital restructuring does not sit independently from the other three macro restructurings underway. It is accelerating all of them.

Labor bifurcation is being driven in part by where capital is flowing. Investment is concentrating in AI-augmented high-skill development and away from entry-level cognitive work, which is structurally shrinking the demand for the workers it used to require. The wage polarization gap is widening because capital is making it wider.

The productivity trough is a direct consequence of front-loaded capital with back-loaded returns. The J-curve in enterprise AI adoption is not just an organizational change management problem. It is built into the capital structure of the investment cycle itself.

Sector stratification at Layer 1, infrastructure, is entirely a function of where capital has concentrated. The migration of value toward Layer 2 and Layer 3 depends on the infrastructure bet paying off. If it doesn’t, the value migration stalls at the layer where the capital already is.

This is the simultaneity problem made visible: the capital restructuring is the engine driving the speed and direction of the other three. Understanding where it goes is not just a financial question. It is the macro economic question of the next several years.

Two Scenarios

The honest framing is not a prediction. It is an acknowledgment that we are at a fork with two plausible paths.

In the first, the infrastructure investment pays off. Enterprise AI adoption accelerates through the productivity trough. Revenue growth follows productivity gains. The $800 billion interest problem resolves because the underlying economics justify the bet. Capital begins to distribute from infrastructure toward platforms and applications. The sectors crowded out today begin to recover access to capital. The pattern follows historical precedent: concentration first, distribution over time.

In the second, the revenue doesn’t materialize on the timeline the debt requires. Enterprise adoption stalls. The productivity-to-revenue gap persists. Credit conditions tighten as the scale of the infrastructure bet becomes harder to justify. Stranded assets accumulate in data centers and chip inventories. The sectors that were crowded out during the concentration phase find themselves emerging into a tighter capital environment, having missed the investment window they needed.

The signals to watch are not the capex announcements. Hyperscalers will continue to report large spending figures regardless of underlying return dynamics, because stopping now would be a more visible admission of a problem than continuing. The announcements are noise. The signals are elsewhere.

Watch how enterprise AI gets priced. The per-seat licensing model that enterprise software has run on for two decades is collapsing under AI’s weight — AI agents don’t map cleanly to seats, and the industry hasn’t landed on a replacement model that customers will accept at the margin required to justify infrastructure costs. That pricing reset is not just a go-to-market problem. It is a revenue recognition problem, and it sits directly in the path between the infrastructure investment and the returns it needs. I wrote about this recently on my Substack newsletter: The CFO calculus behind this shift is worth understanding in more detail.

Watch the application layer. The infrastructure was built for something. Whether Layer 3 applications, the ones that actually automate judgment-intensive workflows rather than assist them, are reaching adoption thresholds that pull through infrastructure utilization is the second key variable. Utilization rates on hyperscaler GPU clusters, not just allocation, are a leading indicator.

And watch the productivity-to-revenue gap. Deloitte’s finding that 66% of organizations see productivity gains but only 20% see revenue growth is not a fixed condition. If the gap begins to close, the scenario improves. If it widens, the arithmetic gets harder.

We are not yet in a position to know which path we are on. That uncertainty is not a reason to dismiss the bet. It is a reason to read the indicators clearly, and not to mistake momentum for resolution. The capital has been committed. What happens next is a function of what the economy does with it.

Next in the series: the labor restructuring. Not the jobs story, but the one underneath it. Who captures the value when AI makes your work more productive, and why the answer matters more than the displacement headlines.

Leave a comment