There is no shortage of AI commentary right now. What there is a shortage of is clarity.

The conversation splits into two camps that talk past each other. One side sees AI as the most transformative technology in human history, a step change that will remake work, wealth, and civilization. The other sees a familiar pattern: overhyped technology, overcapitalized markets, and productivity gains that are always just around the corner. Both camps spend most of their energy arguing about which narrative is correct and very little time looking at what is actually happening in the economy right now.

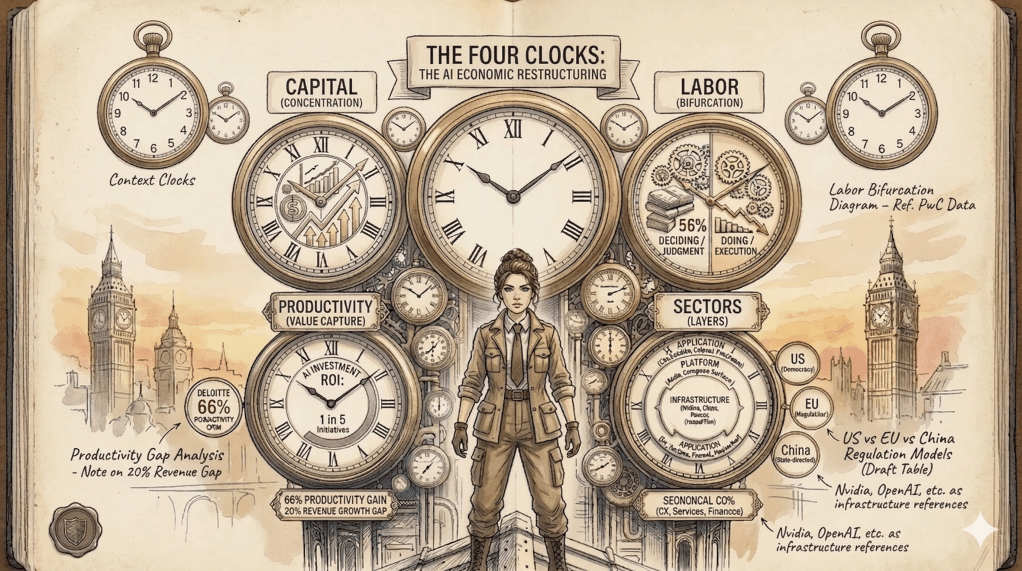

In my time around enterprise software, I’ve been close enough to technology cycles to develop a healthy skepticism about what they deliver and when. What I’m seeing right now isn’t one story. It’s four.

The Premise

There’s a version of this argument that overstates its case, and I want to avoid it. I am not going to argue that AI is historically unprecedented. Every major general-purpose technology, from steam to electricity to the internet, triggered waves of capital concentration, labor disruption, and productivity dislocation before eventually delivering on its promise. The pattern is well-documented. Whether AI follows it, accelerates it, or breaks from it is genuinely uncertain. Anyone claiming to know the answer is selling something.

What I can say is this: the four restructurings underway right now are observable, measurable, and consequential, regardless of where AI ultimately lands in the history books. Some of this analysis is happening in pockets: economists tracking labor, financial analysts tracking capital, consultants measuring productivity, technologists mapping sectors. What seems harder to find is a frame that holds all four together. This is my attempt at one.

Restructuring One: Capital

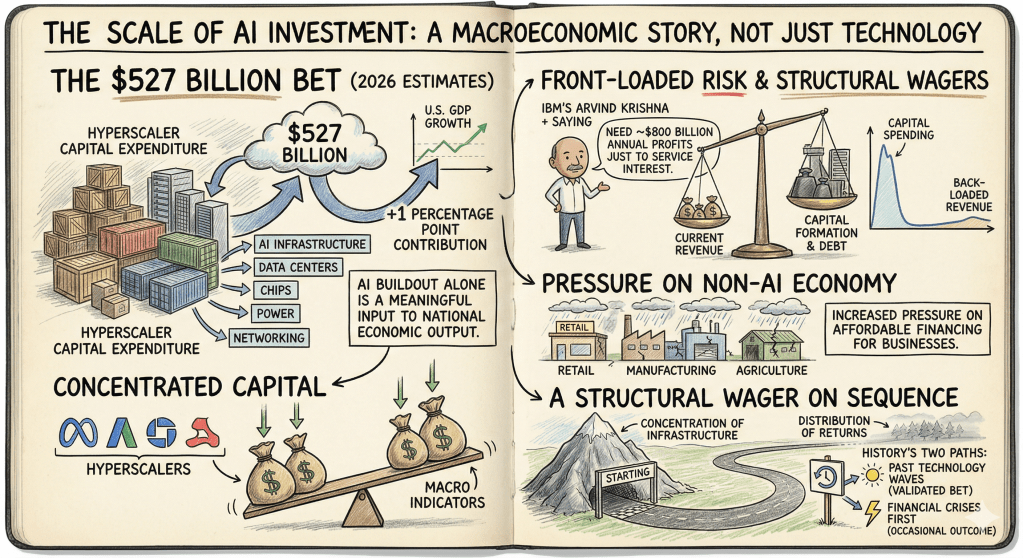

The scale of AI investment is not just a technology story, It is also a macroeconomic one.

In 2026, the consensus estimates for hyperscaler capital expenditure on AI infrastructure, data centers, chips, power, and networking, is $527 billion. That figure is contributing approximately one percentage point to US GDP growth this year. The AI buildout alone is now a meaningful input to national economic output.

The capital is concentrated. A handful of companies are making bets so large that their individual spending decisions move macro indicators. IBM’s CEO Arvind Krishna put it plainly: at current infrastructure investment trajectories, the industry would need roughly $800 billion in annual profits just to service the interest. Whether revenue remotely approaches that level is anyones guess.

This is front-loaded capital formation at historic scale, with very rosy back-loaded revenue assumptions. The pressure on affordable financing for businesses outside the AI infrastructure complex is already measurable with traditional businesses struggling to find affordable financing. The AI bet being made is not just on a technology, it is also a structural wager that concentration of infrastructure before distribution of returns is the right sequence. History has validated that bet in past technology waves. It has also, occasionally, produced financial crises first.

Restructuring Two: Labor

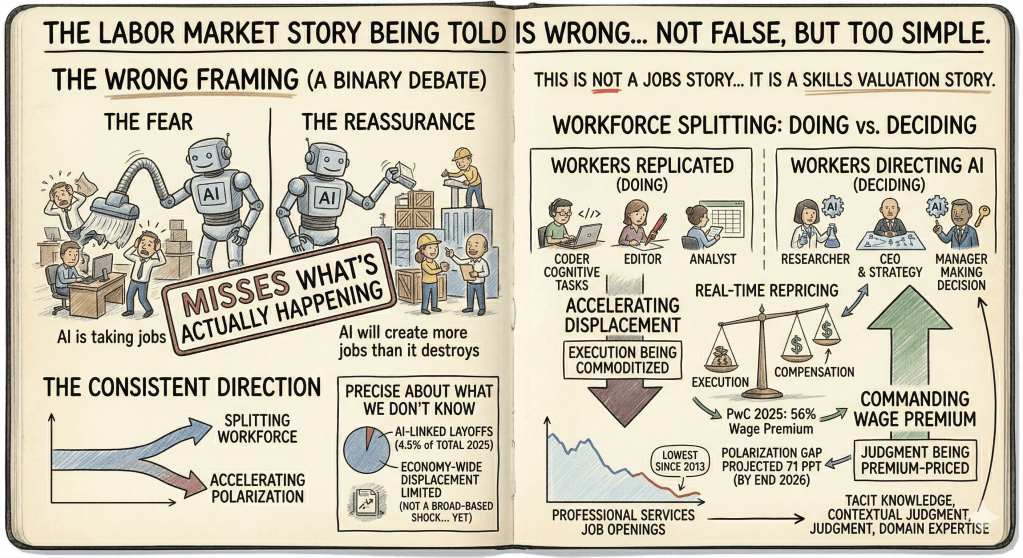

The labor market story being told in most media is wrong, not because it is false, but because it is too simple.

“AI is taking jobs” is the fear. “AI will create more jobs than it destroys” is the reassurance. Both framings miss what is actually happening, which is more precise and more consequential than either.

The data is pointing in a consistent direction: the workforce is splitting in two, along the line between doing and deciding. Workers who can direct AI, who bring the tacit knowledge, contextual judgment, and domain expertise to turn AI output into something usable, are commanding a 56% wage premium according to PwC’s 2025 research. Workers whose cognitive outputs AI can replicate are facing accelerating displacement, with professional services job openings at their lowest since 2013.

This is not a jobs story. It is a skills valuation story.

The economic return on different types of human contribution is being repriced in real time. Execution is being commoditized. Judgment is being premium-priced. The wage polarization gap between these two groups is projected to reach 71 percentage points by end of 2026, compared to 42 points just four years ago.

To be precise about what we don’t know: economy-wide displacement remains limited. AI-linked job cuts accounted for approximately 4.5% of total layoffs in 2025. The disruption is real but concentrated, not yet the broad-based labor market shock that some projections describe. The key word is yet.

Restructuring Three: Productivity

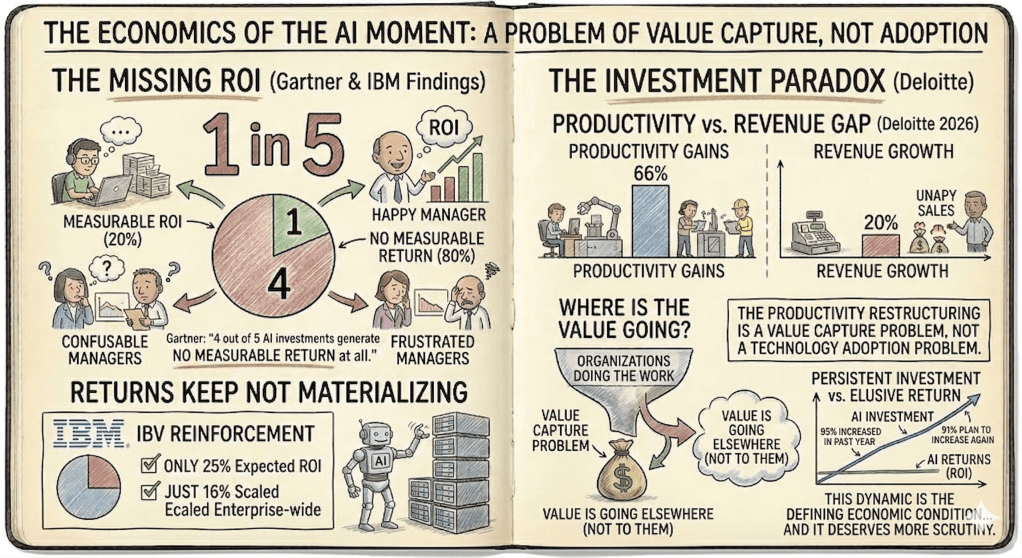

Here is the number that should be getting more attention than it is: 1 in 5.

That is the share of AI initiatives that achieve measurable ROI, according to Gartner’s research. Not modest returns. Not delayed returns. Four out of five AI investments generate no measurable return at all. IBM’s Institute for Business Value arrives at a similar finding: only 25% of AI initiatives have delivered expected ROI, and just 16% have scaled enterprise-wide.

At the same time, Deloitte’s 2026 research finds that 66% of organizations report productivity gains from AI, while only 20% report revenue growth. The gap between those two numbers is not a paradox. It is a signal about where the value is going, and the answer is: not to the organizations doing the work.

Despite all of this, 85% of organizations increased their AI investment in the past year, and 91% plan to increase it again. Capital keeps flowing in. Returns keep not materializing. That dynamic, persistent investment against elusive return, is the defining economic condition of the AI moment right now, and it deserves more scrutiny than it’s getting.

The productivity restructuring is not primarily a technology adoption problem. It is a value capture problem, and I’ll come back to why.

Restructuring Four: Sectors

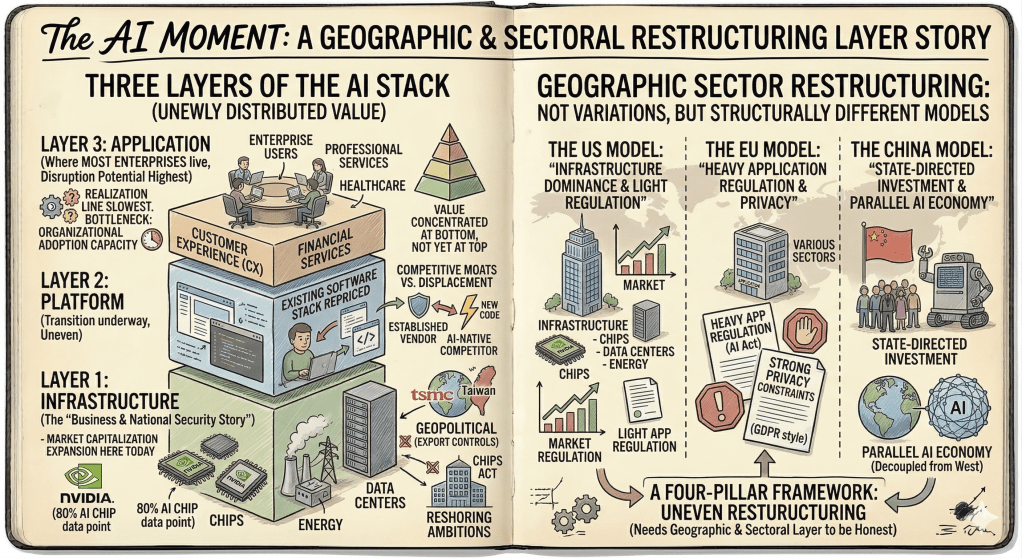

The four-pillar framework needs a geographic and sectoral layer to be honest about how uneven this restructuring actually is.

Think of AI’s economic impact as moving through three layers of an infrastructure stack, and understand that value is currently concentrated at the bottom of that stack, not yet at the top where most enterprises live.

Layer One is infrastructure: semiconductors, energy, data centers. This is where market capitalization expansion is happening today. Nvidia’s approximately 80% share of the AI chip market is one data point. The geopolitical dimension, specifically TSMC in Taiwan, export controls on advanced chips, and the CHIPS Act’s reshoring ambitions, makes this layer structurally complicated in ways that previous technology transitions were not. The infrastructure layer is not just a business story. It is increasingly a national security story.

Layer Two is platform: developer software, cloud infrastructure, developer tools. The existing software stack is being repriced. Some established vendors will absorb AI capabilities and extend their competitive moats. Others will find themselves displaced by AI-native competitors who are not carrying the legacy architecture. This transition is underway, uneven, and far from resolved.

Layer Three is application: customer experience, professional services, financial services, healthcare. This is where most enterprises actually engage with technology, and where the disruption potential is highest. The realization timeline is the slowest of the three layers, because the bottleneck is not technology capability. It is organizational adoption capacity.

The sector restructuring does not follow a uniform path across geographies. The US model (infrastructure dominance, relatively light application regulation so far) looks different from the EU model (heavy application regulation under the AI Act, strong privacy constraints), which looks different still from China’s model (state-directed investment, a parallel AI economy largely decoupled from Western platforms). These are not variations on a theme. They are structurally different versions of the same restructuring.

What Connects All Four

Every major technology wave has produced these four types of restructuring. Capital gets reorganized. Labor markets bifurcate. Productivity dips before it rises. Sectors get reordered from infrastructure out to application.

Steam did it. Electricity did it. The internet did it.

What deserves examination in the current moment is not the nature of any single restructuring. It is the fact that all four are happening at the same time. In previous technology waves, these shifts arrived more sequentially, spaced out enough for institutions, organizations, and labor markets to absorb one before the next arrived. The capital reorganization would largely stabilize before the labor market effects peaked. Sector restructuring would follow productivity gains, not precede them.

AI is compressing all four into the same window. Capital is concentrating while labor is bifurcating while productivity is in its trough while sectors are mid-migration. The macro economic pressure of this moment is not caused by the scale of any single restructuring. It is caused by the compounding effect of four happening at once, each making demands on organizational and institutional capacity that the others are not leaving room to meet.

This is the simultaneity problem. Applied to each of the four pillars individually, it changes what you see. It also keeps the argument honest: the question is not whether AI will eventually distribute value across capital, labor, productivity, and sectors. History suggests it will. The timing, the path, and who bears the cost of getting there are what remain genuinely uncertain.

The Takeaway

Four things are happening simultaneously in the AI economy: capital is concentrating at historic scale, labor markets are bifurcating along the judgment axis, productivity gains are being captured somewhere other than where they are generated, and sector value is migrating through infrastructure layers at different speeds in different geographies.

These are not predictions. They are observable conditions, measurable now, consequential now. Each one warrants a closer look than a single piece allows, and that’s exactly where this is headed. We are all somewhere inside these restructurings, whether we’re tracking them or not. The intent here is to keep pulling the threads apart and make clearer what they mean for the organizations and people navigating them.

My next post in this series dives into the long term impact of capital flows toward hyperscaler infrastructure and the long term impact to the broader global economy. Froma financial perspective, the bet is one of the riskiest in history.

Leave a reply to nitinbadjatia Cancel reply