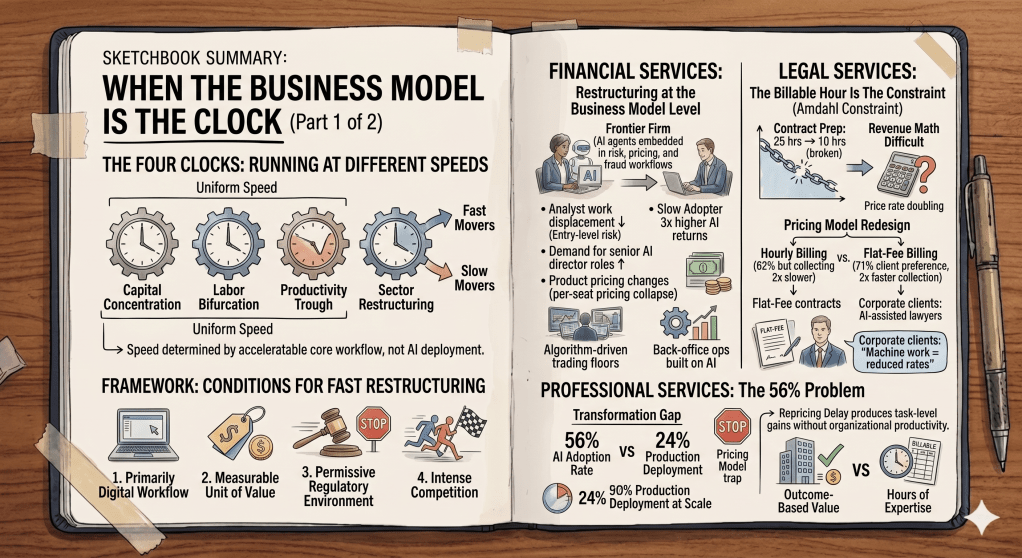

The four clocks in this series have been running at roughly the same speed. Capital concentration, labor bifurcation, and the productivity trough are all happening simultaneously, which is what makes the current moment structurally distinct from previous technology transitions. But the fourth clock, sector restructuring, doesn’t run at a uniform speed across the economy. It runs fast in some industries and slow in others, and the difference is not primarily about how much AI has been deployed. It’s about how much of each sector’s core workflow can actually be accelerated.

I’ve years working at the intersection of customer experience and the enterprise, watching how technology transitions move through industries at different speeds. The pattern is remarkably consistent: the sectors that restructure first are never the ones with the most ‘shiny object’ enthusiasm. They’re the ones where the existing business model creates the most immediate pressure to adapt when productivity changes. The ones that lag are almost always the ones where the accountability structures, the trust requirements, or the physical constraints of the work create a ceiling on how much can be accelerated regardless of tool quality.

Amdahl’s Law, which I’ve covered on my Substack column, applies directly here at the sector level. The sectors restructuring fastest are the ones with the highest proportion of acceleratable workflow. The sectors moving slowest are the ones where physical, regulatory, or trust constraints limit how much of the core work AI can touch. Understanding which sectors are in which category, and why, is the most practically useful question in the AI economy right now for anyone allocating capital, building products, or planning a career.

Part 1 covers the fast movers. They’re not uniformly successful, and the restructuring isn’t uniformly positive. But the structural change in these sectors is already past the point where it can be reversed or meaningfully slowed.

The conditions that drive restructuring

Before looking at specific industries, it’s worth making the underlying logic explicit, because it explains the pattern across everything that follows. This is a framework I’ve arrived at through watching enterprise technology deployments across sectors, and through the advisory conversations I have with companies navigating these transitions. The variable that consistently matters most isn’t the technology. It’s the structure of the business model it lands on.

Sectors restructure fast when four conditions are present:

- First, the core workflow is primarily digital. When the work is information-intensive and the existing infrastructure is already built on data, AI has maximum surface area to work with.

- Second, the business model has a clear, measurable unit of value. When it’s obvious what the sector is selling and how it’s priced, AI-driven productivity changes create immediate pressure on that pricing, which forces business model adaptation faster than in sectors where value is diffuse or harder to quantify.

- Third, the regulatory environment allows for workflow change without requiring years of clinical trials, public procurement cycles, or legislative action.

- Fourth, the competitive dynamics are intense enough that firms that don’t adapt lose customers to firms that do, on a timeline short enough to be existential.

Financial services, legal, and professional services all meet most of these conditions. The restructuring underway in each of them is distinct in character, but it’s driven by the same underlying logic.

Financial Services: Restructuring at the Business Model Level

Financial services has moved further into AI-native operations than any other major sector, and the restructuring is no longer happening at the tool adoption level. It’s happening at the business model level.

An IDC study from late 2025 identified a category it calls Frontier Firms: financial institutions where AI agents are embedded across every major workflow, blending human judgment with AI capabilities across risk decisioning, pricing models, customer engagement, and fraud detection at scale. These firms report returns on their AI investments roughly three times higher than slow adopters. The gap between AI leaders and laggards in financial services is no longer a capability gap. It’s a compounding competitive gap, and it’s widening.

The workflow characteristics explain why. Financial services is almost entirely digital at its core. The product is information-based, the delivery is digital, the customer relationship is mediated through data, and the risk decisions that determine profitability are exactly the kind of pattern-recognition-at-scale work that AI is most effective at. The proportion of the sector’s core workflow that can be accelerated is among the highest of any industry.

This creates a direct labor restructuring inside financial services that is already well advanced. Trading floors have been restructuring for a decade under algorithmic automation. Research departments are contracting as AI-generated analysis displaces entry-level analyst work. Back-office operations, compliance monitoring, and fraud detection are being rebuilt around AI systems rather than around human reviewers. The labor bifurcation from the earlier pieces in this series is arguably most visible here: the demand for workers who can direct and evaluate AI systems at the senior level is high, and the demand for workers who perform the tasks those systems now handle is falling structurally.

The capital piece in this series noted that the per-seat pricing model in enterprise software is collapsing under AI’s weight, a shift I’ve written about separately and watched play out in real time across the CX software space. Financial services is experiencing its own version of that pricing problem at the product level. When AI enables a bank to price risk more accurately, personalize offers more precisely, and detect fraud more reliably, the products themselves change. The competitive advantage shifts from balance sheet size and branch network to data quality and AI infrastructure, which is a different kind of capital intensity altogether.

Legal Services: When the Business Model Is the Constraint

Legal services is undergoing the most structurally visible restructuring of any professional sector, because the constraint being broken is not a workflow constraint. It’s the business model itself.

The billable hour is the Amdahl constraint of legal services. It is the non-acceleratable component that limits how much AI-driven efficiency can translate into firm revenue. When AI reduces the time required to prepare a contract from 25 hours to 10, the math becomes immediately difficult: to generate the same revenue at the same hourly rate, the firm would need to raise its rate to more than double the previous level. Clients that now understand exactly how much AI has accelerated the work are not paying doubled rates for work that took half the time.

Corporate clients are moving fast on this. UBS updated its billing guidelines in early 2026 with AI-specific provisions. The message from major corporate legal departments is converging: if a machine can do the work, the client is not paying a lawyer’s full hourly rate for it. 71% of legal consumers now prefer flat-fee billing, and firms billing with fixed fees collect payment nearly twice as fast, yet 62% of legal work still operates under hourly billing.

The direction of travel is clear. Alternative fee arrangements are forecast to rise from 20% of law firm revenue in 2023 to over 70% by 2025 across AI-native and AI-forward firms. Allen and Overy reported a 23% increase in profit per partner within 18 months of shifting 40% of contract work to AI-augmented fixed-fee pricing. The firms willing to restructure their pricing model in response to AI-driven efficiency are capturing margin that hours-based firms are leaving behind.

The legal sector restructuring connects directly to the labor pipeline piece from earlier in this series. Document review, contract drafting, legal research, and due diligence are the entry-level cognitive work of the legal profession. They are also the work AI is absorbing fastest. The same hollowing-out of the career ladder described in Part 2 of the labor series is happening in law with particular speed. Big law firms have already cut new associate hiring meaningfully, and the pipeline of junior lawyers who would have built expertise through years of exactly that work is narrowing.

The restructuring is not uniformly negative. Firms that genuinely redesign around AI are producing better work faster, with fewer errors, and at prices that clients find more predictable. The productivity piece in this series argued that organizational productivity requires workflow redesign, not just tool adoption. Legal services is providing one of the clearest live examples of what that redesign looks like in practice, and what it costs in terms of business model adaptation.

Professional Services: The 56% Problem

Professional services beyond legal (consulting, accounting, advisory, and related fields) present a more nuanced picture than either financial services or legal. Adoption is high. Real transformation is less advanced than the adoption numbers suggest. This is the sector I watch most closely from my own vantage point, because it’s where many of the conversations I have with enterprise technology buyers are happening. The pattern I hear consistently is some version of: we’ve deployed the tools, our people are using them, and we’re not yet sure what to do about the fact that the work takes less time now.

Professional services has a 56% AI adoption rate as of 2025, the highest among knowledge-intensive sectors. But only 24% have reached production deployment at scale. The gap between 56% and 24% is the most important number in the sector, and its explanation illuminates why adoption and transformation are not the same thing.

The constraint is the same one facing legal: the pricing model. Professional services firms bill primarily on time and expertise. When AI makes the time component shorter and the expertise component partially replicable, the billable unit loses its foundation. Unlike legal, which is being pushed hard from the client side, professional services firms have more control over the pace of repricing because client sophistication varies more widely. That control is also a trap: it allows firms to delay the business model adaptation while deploying the tools, which produces exactly the kind of task-level productivity without organizational productivity transformation that the productivity piece described.

The firms that are pulling ahead are the ones treating AI as a reason to redefine their value proposition, not just as a reason to do the same work faster. The transition from “we provide hours of expertise” to “we provide outcomes” requires the workflow redesign Stanford’s Enterprise AI Playbook identified as the distinguishing characteristic of high-performing AI organizations. In professional services, that redesign is also a repricing, a reconfiguration of the client relationship, and a fundamental change in how value is measured. Most firms haven’t completed that work. The ones that have are not just more productive. They’re competing differently.

How the Fast Movers Connect to the Other Three Clocks

The sector restructuring in financial services, legal, and professional services isn’t happening independently of the capital, labor, and productivity restructurings. It’s the downstream consequence of all three running simultaneously.

Capital concentration in AI infrastructure is accelerating the competitive gap between sector leaders and laggards. The Frontier Firms in financial services that are pulling ahead aren’t just using better tools. They’re accessing capital, talent, and infrastructure that is concentrating in the same direction the $527 billion buildout is pointing. Firms without the data infrastructure, the technical talent, or the balance sheet to compete at the infrastructure layer are increasingly competing for position at the application layer, where their existing client relationships and domain expertise still count. The window for that positioning to be durable is not infinite.

The labor bifurcation is most advanced in these three sectors, for the same reason the sector restructuring is most advanced: the workflows are most acceleratable, so the displacement of entry-level cognitive work is furthest along. The conversion mechanism problem from the labor series, the absence of organizational infrastructure for translating AI productivity gains into worker compensation, is playing out here with the added complexity of business model change. It’s not just that firms haven’t designed a way to share AI productivity gains with their workers. It’s that the definition of what the work is worth is being renegotiated in real time.

And the productivity lesson is most clearly visible here. The legal firms that are actually capturing margin from AI are the ones that redesigned their pricing model, not the ones that just gave associates better tools. The financial services firms generating 3x returns are the ones where AI is embedded across the workflow, not layered on top of it. The professional services firms stuck at 56% adoption without production deployment are the ones that haven’t done the workflow redesign. Amdahl’s Law at the sector level looks exactly like Amdahl’s Law at the organizational level.

What the Fast Movers Reveal

The sectors restructuring fastest are teaching the rest of the economy something important: the technology is not the constraint. The business model, the workflow design, and the organizational willingness to redesign around AI are the constraints. Where those constraints have been addressed, the restructuring is real and the competitive divergence is already compounding. Where they haven’t, tool adoption produces incrementally faster versions of existing processes, and the productivity gap relative to sector leaders widens.

What I find most striking about the fast movers is not the productivity gains. It’s how quickly the conversation inside those organizations has shifted from “how do we implement AI” to “how do we price and deliver value differently.” That shift is the real indicator that structural change is underway. As long as the conversation stays in the implementation frame, you’re still in the adoption phase. The restructuring starts when the business model question becomes unavoidable.

That lesson is transferable. Part 2 of this piece covers the sectors on a longer timeline. The reasons they’re slower are structural, not technological. But the pattern of what it takes to actually restructure, as opposed to just adopting, is identical.

Part 2: Where the Clocks Run Slower. Healthcare, manufacturing, and the public sector are on longer timelines for reasons that have nothing to do with AI capability and everything to do with regulatory structures, physical constraints, and the specific nature of the trust requirements in each industry.

Leave a comment