Part 1 of the sector clock established that the sectors restructuring fastest share a common profile: digital-native workflows, clear and measurable units of value, relatively low regulatory barriers to workflow change, and competitive dynamics intense enough to punish non-adoption on a short timeline. Financial services, legal, and professional services meet most of those conditions. The restructuring in those sectors is advanced, compounding, and past the point of reversal.

The sectors in Part 2 don’t fit that profile. And I want to be direct about something before we get into the analysis: slower restructuring doesn’t mean less consequential. Healthcare, manufacturing, and the public sector together represent the larger share of the economy, employ more people, and have more direct impact on human welfare than the fast-moving knowledge sectors in Part 1. The fact that they’re on a longer timeline isn’t a reason to pay them less attention. It may be a reason to pay them more. Healthcare, manufacturing, and government and education are restructuring more slowly, and the gap between AI adoption rates and meaningful structural transformation is larger. But the reason isn’t that the technology doesn’t apply. AI has demonstrable value in all three sectors. The reason is that the constraints limiting transformation aren’t workflow constraints in the ordinary sense. They’re physical, regulatory, or accountability constraints that AI can’t accelerate around.

Amdahl’s Law again: the performance improvement of any system is limited by the portion that cannot be enhanced. In these sectors, the non-acceleratable portion is large, structural, and not going away on a short timeline. That shapes everything: the pace of adoption, the nature of the returns, and the kind of organizational redesign that’s actually possible.

Healthcare: The Clinical-Administrative Divide

Healthcare is one of the most consequential sectors for AI transformation, and one of the most complicated to think about clearly. I’ve spent limited time in this space from the customer experience side, but this much I understand: patient experience is one of the most demanding CX domains in enterprise software, precisely because the stakes of a poor experience aren’t just churn. They’re clinical outcomes. That context shapes how I think about the AI transformation question here, and why I think the distinction that gets most consistently collapsed in coverage is the most important one to hold onto: the difference between administrative AI and clinical AI.

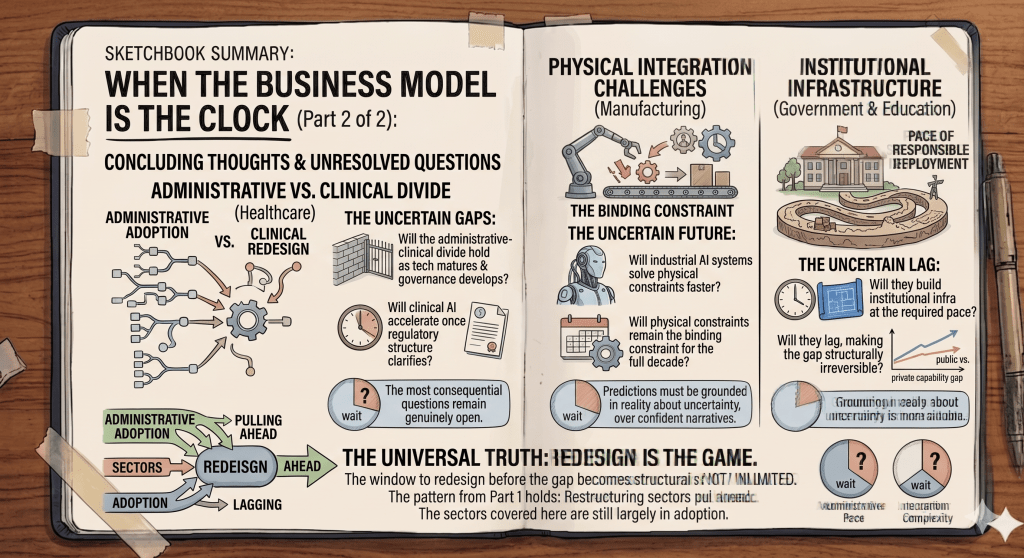

Administrative AI in healthcare is already transforming operations. Scheduling, billing, documentation, prior authorization, coding, and claims processing are all primarily digital, primarily information-based, and relatively low in trust requirements compared to clinical work. These are the workflows where Amdahl’s constraint is smallest: most of the work is acceleratable (is that word?), and the regulatory and liability barriers are manageable. Healthcare is adopting AI at twice the rate of the broader economy when administrative applications are included in the count.

Clinical AI is a fundamentally different category. Diagnosis, treatment decisions, medication management, surgical assistance, and care coordination involve workflows where the non-acceleratable portion is very large: the physical examination, the patient relationship, the clinical judgment built over years of practice, and the liability and regulatory framework that governs all of it. The trust requirement in clinical AI is not simply higher than in administrative AI. It’s structurally different. An error in a billing workflow costs money. An error in a clinical decision costs lives, and the legal and regulatory consequences are correspondingly severe.

This creates a structural two-speed dynamic inside healthcare. Administrative transformation is happening now and at real scale. Clinical transformation is happening at the edges (diagnostic imaging AI is the clearest example, where AI is genuinely improving accuracy) and will take significantly longer to reach the core of clinical workflow. The governance structures, regulatory frameworks, and liability models that would be required for deep clinical AI transformation are still being built: by mid-2025, over 250 healthcare AI bills had been introduced across more than 34 states, with no consistent federal framework in place.

The capital piece in this series is directly relevant here. Healthcare investment fell 12% year over year in 2025 while AI took 46% of what remained. Biopharma investment fell 19%. The capital crowding-out effect described in that piece isn’t an abstract macro concern for healthcare. It’s a present constraint on the sector’s capacity to fund the research, the clinical trials, and the infrastructure development that deep transformation requires. Healthcare is being asked to restructure at the same time that the investment pool it needs to do so is being compressed by AI’s gravity on capital markets.

The result is a sector in genuine transition at the administrative layer, moving much more cautiously at the clinical layer, and facing a capital environment that isn’t making either easier. Shadow AI has already proliferated, with clinical staff adopting AI tools informally across organizations that lack governance frameworks for them. That’s both a signal that demand is real and a warning that the structural elements required for safe, scalable deployment haven’t been built yet.

Manufacturing: The Physical Constraint Problem

Manufacturing presents a different puzzle from the other sectors in this piece, and honestly the one I find most analytically interesting in this series. The data says AI transformation in manufacturing has the highest ROI of any sector, with companies reporting a 200% average return on AI investments and a typical payback period of just 1.2 years. Factories that close the gap between exploration and deployment are achieving productivity gains of 20% to 30%, cutting machine downtime by up to 50%, and reclaiming 25% on energy costs. These are not marginal improvements.

Yet transformation is slower than the ROI numbers suggest it should be. More than 60% of manufacturing companies have developed an AI strategy, but the share of industrial manufacturers who have highly automated key processes sits at 18%. That is expected to rise to 50% by 2030, which is meaningful progress, but on a timeline that tells you something important about the physical constraint problem.

Manufacturing workflows are not primarily digital. They are physical, and the physical components can’t be accelerated in the same way information can. AI can predict when a machine will fail, and that prediction is enormously valuable. But it doesn’t fix the machine faster. AI can optimize a supply chain routing decision in milliseconds. But the physical logistics of moving goods through the world operate on the timeline of ships, trucks, and warehouses, not algorithms. The digital-physical integration problem, building the sensor infrastructure, the connectivity, and the data pipelines that give AI systems real-time visibility into physical processes, is the non-acceleratable portion of manufacturing transformation. It requires capital investment in physical infrastructure, not just software deployment.

This explains both the high ROI and the slower adoption pace. The ROI is high because when AI is successfully integrated into manufacturing workflows, it’s touching processes where small efficiency gains have large dollar consequences: unplanned downtime in a factory costs orders of magnitude more than unplanned downtime in a software team. The adoption pace is slower because the integration work is physically complex, capital-intensive, and not as easily reversed if it doesn’t work as a software rollout would be.

The labor dynamics in manufacturing are also structurally different from the knowledge sectors covered in Part 1 and in the earlier labor pieces. Manufacturing has been automating physical tasks for decades. The workforce implications of AI are layered on top of an already-restructured labor landscape, rather than arriving as a first disruption. The current AI wave is most directly affecting the supervisory, analytical, and technical roles that manage and optimize automated physical processes, not the physical labor itself. That creates a different bifurcation pattern from knowledge work: the premium is going to workers who can operate at the intersection of physical systems and AI-driven optimization, which is a specific and relatively scarce skill set.

PwC’s 2026 industrial manufacturing outlook found that the gap between manufacturing AI leaders and laggards is widening, with leaders more than doubling automation of key processes expected by 2030. That divergence is the manufacturing version of the Frontier Firms gap in financial services: the structural advantage of early movers is compounding in ways that will be difficult for laggards to close.

Government and Education: The Accountability Constraint

Government and education are the slowest-moving sectors in the AI restructuring, and the reasons are less about the technology and almost entirely about the accountability structures that govern both. I’ll admit this is the section where my enterprise software background is least directly applicable. These aren’t sectors I’ve worked inside the way I have financial services or healthcare. But the pattern I observe from the outside is consistent with what I’ve seen in every other technology transition: the sectors where failure has the most asymmetric consequences are always the ones that move most carefully, and usually for good reason.

Government and education are not primarily market-competitive environments. They don’t lose customers to competitors in the way that law firms or banks do when they fall behind on AI adoption. The incentive structure that accelerates transformation in market-competitive sectors doesn’t apply in the same way. The timeline on which transformation becomes existentially necessary is measured in political cycles and institutional change processes, not competitive market quarters.

There’s also a trust and accountability requirement in both sectors that has no direct equivalent in private sector AI deployment. When a government agency uses AI in a decision that affects a citizen’s benefits, immigration status, housing application, or criminal proceeding, the accountability requirements are fundamentally different from when a bank uses AI to price a loan. Colorado’s AI Act, which kicks in for enforcement in June 2026, requires disclosure whenever AI is used in high-risk decisions, annual impact assessments, anti-bias controls, and multi-year record-keeping. Nearly every state, as well as the federal government, is attempting to ‘regulate’ AI. The jury is out on the real impact, either negative or positive, that these initiatives will have. But, the speed of AI-driven decision-making will likely require some sort of public guardrails.

Education has a parallel trust requirement with different characteristics. The question of how AI should interact with the learning process, whether it accelerates understanding or substitutes for it, whether it helps students develop judgment or develops a dependency that undermines it, is genuinely unresolved. It’s not a question that can be answered by adoption data. The administrative layer of education (scheduling, resource allocation, student support services) is restructuring on a timeline similar to healthcare’s administrative layer. The instructional core is on a much longer timeline, from what I can tell.

What’s worth watching in both sectors is not the headline adoption rate but the institutional infrastructure being built around AI deployment: the governance frameworks, the audit requirements, the accountability models, and the procurement processes. These are the non-acceleratable components. They can be built faster or slower, with more or less deliberateness, but they can’t be skipped. The sectors that are investing in building this infrastructure now, rather than waiting for a crisis to force it, will be significantly better positioned when the technology matures to the point where deep structural deployment becomes viable.

The Simultaneity Problem at the Sector Level

The anchor piece in this series introduced the simultaneity problem: AI is compressing four restructurings that historically arrived sequentially into a single window. The sector analysis in both parts of this piece illustrates what that compression looks like from the inside of each industry.

Financial services is running all four clocks at near-maximum speed simultaneously: capital concentration reshaping infrastructure, labor bifurcating rapidly, productivity restructuring already advanced, and sector business model transformation underway. Healthcare is running the capital clock (being crowded out), the labor clock (administrative bifurcation), and the beginning of the productivity clock, while the sector restructuring clock at the clinical level barely registers yet. Manufacturing is running the productivity and sector clocks relatively effectively, while the labor clock runs on a different track than knowledge sectors and the capital clock is constrained by physical infrastructure investment cycles.

There is no sector where all four clocks are fully synchronized. There is no sector that is unaffected by all four. The variation between industries is itself a signal about where value will accumulate, where disruption will be most intense, and where the timeline for organizational adaptation is most urgent.

What We’ll Know in Five Years That We Can’t Know Now

The honest conclusion of both parts of this sector piece is that some of the most consequential questions are genuinely open. I started this series wanting to write something more definitive, and the research kept pushing back. The data is clear on what’s happening now. It’s much less clear on how it resolves. I’ve come to think that grounding predictions in reality about that uncertainty is more valuable than the confident narratives that tend to dominate AI coverage in both directions.

We don’t yet know whether healthcare’s administrative-clinical divide will hold as the technology matures and governance frameworks develop, or whether clinical AI will begin moving faster once the regulatory structure clarifies. We don’t know whether manufacturing’s physical integration challenges will be solved faster by the next generation of industrial AI systems or will remain the binding constraint for the full decade. We don’t know whether government and education will build the institutional infrastructure for responsible AI deployment at the pace the technology’s development is demanding, or whether they’ll lag so far behind that the gap between public and private sector capability becomes a structural problem in its own right.

What we do know is that the pattern from Part 1 holds at every level of analysis: the sectors, organizations, and roles that are restructuring around AI are pulling ahead of those that are adopting without restructuring. Adoption is the entry point. Redesign is the game. And the sectors covered in Part 2 are still largely in the adoption phase, while the window for the redesign work to happen before the gap becomes structurally irreversible is not unlimited.