Part 2 of 2: The Labor Clock

This is Part 2 of a two-part piece on the labor restructuring underway in the AI economy. Part 1 covered the bifurcation already visible in current data and the historical pattern of who captures productivity surpluses. This piece goes underneath that, to a structural problem that moves on a longer timeline and will be significantly harder to address once it becomes legible.

The displacement conversation focuses on workers who have jobs today and may not have them tomorrow. That’s a real and serious concern, and the data behind it isn’t trivial.

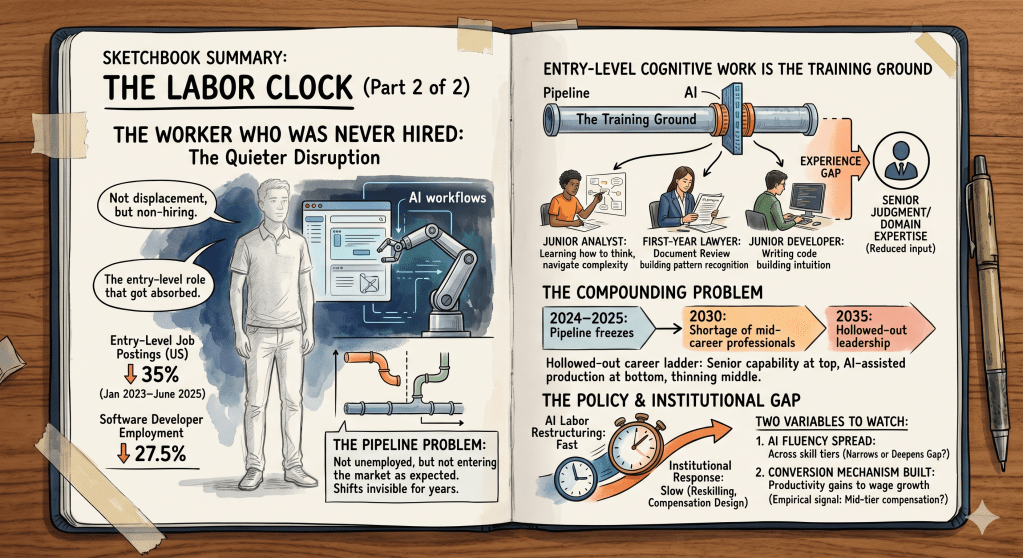

But there’s a version of the labor disruption that’s quieter, slower, and in some ways more consequential: not the worker displaced, but the worker who was never hired. The junior analyst position that wasn’t posted. The entry-level legal researcher role that got absorbed into an AI workflow. The new graduate who couldn’t find a foothold in the first rung of a career ladder that has quietly lost a rung.

This is the pipeline problem. It doesn’t show up cleanly in unemployment data, because the people affected aren’t unemployed. They’re simply not entering the labor market in the ways they expected to. Aggregate job numbers stay relatively stable while the composition underneath them shifts in ways that won’t be fully visible for years.

Entry-Level Cognitive Work Is Not Just Employment

To understand why this matters, you have to understand what entry-level cognitive work actually does in an economy. The answer isn’t just “provides jobs.” It provides something more structural: it’s the training ground where workers develop the judgment, contextual pattern recognition, and accumulated experience that makes mid-career and senior cognitive work possible.

A junior analyst doesn’t just produce analysis. She learns, through exposure and iteration and feedback, how to think about a problem, how to navigate organizational complexity, how to identify what matters in a dataset. A first-year lawyer doing document review isn’t just reviewing documents. He’s building the foundational pattern recognition that eventually makes him capable of running a negotiation or structuring a deal. A junior software developer writing routine code is building intuition about how systems fail, how edge cases behave, how to read someone else’s architecture. That intuition doesn’t transfer from a tutorial.

When AI absorbs the production layer of that work, the training ground shrinks with it. Not because organizations intend to underinvest in junior talent development. The mechanism by which that development happened (doing the actual work, making actual mistakes, being corrected, doing it again) has simply been interrupted.

Where the Pipeline Is Already Narrowing

This isn’t a theoretical future risk. The pipeline compression is visible in current data across multiple fields.

Entry-level job postings in the United States fell 35% between January 2023 and June 2025. In software development specifically, overall programmer employment fell 27.5% between 2023 and 2025. Big technology companies reduced new graduate hiring by 25% in 2024 compared to 2023. At AI-adopting firms more broadly, headcount for early-career roles has fallen 7.7% over six consecutive quarters since early 2023.

These aren’t anomalies in a single sector. They’re a consistent directional signal across legal research, financial analysis, software development, basic consulting work, and customer operations: the fields that have historically served as the primary entry points for college-educated workers into professional careers.

The work itself still needs to get done. What’s changing is who does it, and in what capacity. AI tools are handling the production layer. The remaining human role is moving toward oversight, quality control, edge case judgment, and interpretation. Those are genuinely valuable functions. They’re also not the functions through which workers have traditionally built the deep domain expertise that makes them valuable at senior levels.

The architecture of the talent pipeline is being restructured faster than the institutions responsible for managing it (employers, universities, professional organizations) have recognized or responded to.

The Compounding Problem

Infrastructure underinvestment compounds. This is true of physical infrastructure: the bridge that isn’t maintained becomes the bridge that fails, at a cost far larger than the maintenance would have required. It’s equally true of human capital infrastructure.

The workers who don’t enter the pipeline in 2024 and 2025 aren’t just absent from the workforce now. They’re absent from the pool of mid-career professionals in 2030 and senior professionals in 2035. The skills, judgment, and contextual expertise that would have developed through a decade of professional experience don’t materialize on an alternative timeline. They simply don’t exist.

Technology industry leaders have started naming this concern directly. When entry-level work disappears, the expectation shifts to junior workers arriving already capable of functioning at a higher level, without having had the institutional experience that would have made that possible. The result, over time, is a hollowed-out career ladder: senior capability at the top, AI-assisted production at the bottom, and a thinning middle where accumulated human expertise used to reside.

The timeline on which this becomes a visible problem is long enough to be easy to dismiss today. That’s precisely what makes it structurally dangerous. The decisions being made right now about junior hiring, entry-level workflow design, and early career development will determine the talent supply of the early 2030s. By the time the gap is obvious, the window for addressing it at reasonable cost will have closed.

The Policy Gap

The restructuring is moving faster than the institutional response. That observation doesn’t require a position on what the right response should be. It’s simply a description of the current timing mismatch.

Reskilling and workforce development programs operate on multi-year timelines, require significant coordination between employers, educational institutions, and government, and have a mixed track record even under favorable conditions. The AI labor restructuring isn’t operating on that kind of patient, sequential timeline. It’s moving simultaneously across multiple sectors, compressing changes that previous technology transitions spread over a decade or more into a much shorter window.

The same is true of the compensation infrastructure. The conversion mechanism for turning AI productivity gains into wages, described in Part 1, is an organizational design problem. Building it requires companies to deliberately rethink how job scope, performance evaluation, and compensation adjustment work in an AI-augmented environment. That’s not a fast process under the best conditions, and most organizations haven’t started it yet.

That’s the simultaneity problem applied specifically to labor: the restructuring of entry-level work, the bifurcation of wages, the compression of the talent pipeline, and the absence of a functioning conversion mechanism to share productivity gains, all happening at the same time, faster than the feedback loops that would normally trigger a response.

This piece isn’t a prescription for what the response should be. Reasonable people with different frameworks for how labor markets should function will reach different conclusions. What isn’t reasonable is assuming the response will arrive on its own, at the right time, without deliberate effort to close the gap between the speed of the restructuring and the speed of the institutional capacity to address it.

Two Variables to Watch

The labor restructuring, across both parts of this piece, resolves around two variables that will be visible before the full structural impact becomes clear.

The first is how fast AI fluency spreads across skill tiers. The current bifurcation is driven in part by an uneven distribution of AI capability: workers in higher-skill roles have better access to tools, better organizational support, and better ability to integrate AI into complex judgment work. If that distribution broadens over the next several years, the wage gap could narrow and the pipeline problem could partially self-correct. If it narrows further, if AI fluency becomes even more concentrated at the top, the bifurcation deepens.

The second is whether the conversion mechanism gets built. Part 1 made the case that the organizational infrastructure for turning AI productivity gains into wage growth is largely absent right now. The empirical signal to watch is whether that changes: specifically, whether productivity improvements visible in industry-level data start translating into compensation growth across AI-exposed roles, not just for senior workers who already have negotiating leverage, but for the mid-tier workers where the bifurcation is sharpest. If organizations begin proactively redesigning how job scope and compensation are connected in an AI-augmented environment, the gains could start flowing through. If the gains keep showing up in margin data without passing through to wages, the conversion mechanism isn’t being built, and the structural gap widens.

These two variables won’t resolve quickly. But they’re measurable, and they’ll be leading indicators of which direction the labor clock is actually pointing.

Next in the series: the productivity restructuring. The J-curve in enterprise AI adoption isn’t just a change management problem. It’s built into the economics of how the technology was deployed. What that means for organizations navigating it now, and what the data says about when and how it resolves.

One response to “The Workers Who Were Never Hired”

[…] The Workers Who Were Never Hired Who Gets Paid When the Machine Does the Work? Front-Loaded: The Economic Cost of AI’s Capital Concentration AI’s running in four different races. We’re in all of them […]

LikeLike