Part 1 of 2: The Labor Clock

This is a two-part piece. The labor restructuring is the most layered of the four clocks in the AI economic reconfiguration, so I’m breaking this up into two parts. Part 1 covers what the data already shows: who is capturing the productivity surplus, and why the bifurcation happening right now looks structural rather than transitional. Part 2 goes underneath that, to a slower-moving problem that won’t show up in today’s employment numbers but will be significantly harder to address once it does.

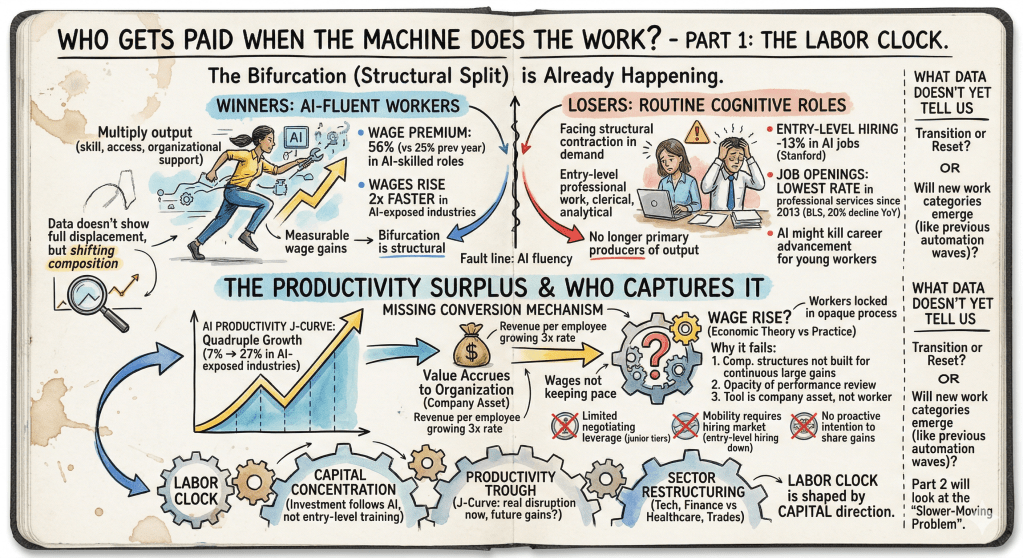

The productivity story gets told as a win. AI is making workers faster, smarter, more capable. That part is true. ~PwC’s 2025 Global AI Jobs Barometer~ found that industries most exposed to AI saw productivity growth nearly quadruple: from 7% between 2018 and 2022 to 27% between 2018 and 2024. Revenue per employee in the most AI-exposed industries is now growing at three times the rate of the least exposed.

That’s a real and significant shift. But the headline doesn’t answer the most important question: who actually captures the gains?

The Bifurcation That’s Already Happening

The labor market isn’t waiting for AI to mature before it starts restructuring. The split is already visible in current data, and it runs along one fault line: AI fluency.

Workers who use AI to multiply their output (those with the skill level, the role access, and the organizational support to integrate AI into their core work) are seeing measurable wage gains. ~PwC’s data~ puts the wage premium for AI-skilled roles at 56% over comparable roles that don’t require AI skills, up from 25% the year before. Wages are rising twice as fast in AI-exposed industries compared to those least exposed.

On the other side of the fault line, the picture looks very different. Workers in routine cognitive roles, the analytical, clerical, and entry-level professional work that knowledge economies have relied on for decades, are facing a structural contraction in demand. Not a temporary dip. ~The Stanford Digital Economy Lab~, using ADP employment data, found that entry-level hiring in AI-exposed jobs has dropped 13% since large language models began proliferating. In January 2025, the Bureau of Labor Statistics reported ~the lowest rate of job openings in professional services since 2013~, a 20% year-over-year decline.

This isn’t the full displacement story that dominates the public conversation. Aggregate employment in AI-exposed occupations hasn’t collapsed. But the composition is shifting: toward workers who can direct, evaluate, and extend AI outputs, and away from workers whose primary contribution was producing those outputs in the first place.

The bifurcation is real, it’s measurable, and it’s accelerating.

The Productivity Surplus and Who Captures It

When a worker becomes 30% more productive because of a tool they use at work, economic theory suggests their wage should rise accordingly. But productivity gains don’t automatically become wages. There’s a conversion mechanism in between, and right now that mechanism is largely missing.

That mechanism, in larger organizations, looks like this: a performance review that recognizes AI-enabled output as a basis for better pay. A job classification system that accounts for expanded scope when a worker’s effective capacity doubles. A renegotiation cycle where the worker can credibly say “I now do significantly more than my role was originally scoped for.” In practice, most enterprise compensation structures weren’t built for any of that as an on-going process. They were built for a world where productivity gains were incremental, hard to attribute to a single tool, and distributed across teams and departments over years.

AI productivity gains are none of those things. They’re often substantial, they’re attributable to a specific tool the company owns and licenses, and they’re arriving fast. The organizational machinery for converting them into better pay simply hasn’t caught up.

This matters because of a structural fact that tends to get overlooked: the AI tool is a company asset, not a worker asset. When a worker uses it to produce more, the productivity gain accrues first to the organization that deployed it. The worker’s portion is locked into an opaque compenstaion review process, which isn’t even well documented. One other option is through mobility to a competitor that will pay more for their AI-augmented output. Most growth companies use the stock/equity lever as a way to reward, but there’s no guarantee on liquidity or value there as well. At the entry and mid tiers where the bifurcation is sharpest, none of those pathways are reliably open. Entry-level workers have limited negotiating leverage. Mobility requires a market that’s hiring, and the data on entry-level hiring is moving in the wrong direction. And organizational intention to proactively share AI productivity gains with junior workers is not something the available evidence suggests is widespread.

The productivity gains are real. The problem isn’t that they don’t exist. It’s that the conversion mechanism to turn them into compensation is broken, absent, or yet to be designed at most organizations. And until that changes, the gains will keep showing up in margin data before they show up in wage data, if they show up in wage data at all.

How Labor Connects to the Other Three Clocks

The labor restructuring isn’t running independently from the other three macro restructurings. It’s being actively shaped by them.

Capital concentration, covered in the previous piece in this series, is a direct input to labor bifurcation. Investment is flowing toward AI infrastructure and AI-augmented high-skill development, and away from the roles, training pipelines, and institutional frameworks that sustain entry-level and mid-tier cognitive work. That’s not a neutral technological outcome. It’s a consequence of where capital has chosen to go.

The productivity trough, the well-documented J-curve in enterprise AI adoption where investment precedes measurable returns, has a labor-side mirror. Organizations in the trough are simultaneously deploying AI tools, restructuring workflows, and absorbing the transition costs of both. The workers navigating that transition are experiencing real disruption without yet seeing the productivity gains that are supposed to follow. When the gains do arrive, the value capture question becomes immediate: does the organization translate them into wages, or into margins?

Sector restructuring, the fourth clock, determines which industries experience labor displacement first and which absorb it most slowly. Technology, finance, legal services, and professional consulting are already deep into the restructuring. Healthcare, education, and trades are moving more slowly, for reasons that are partly regulatory, partly physical, and partly about the nature of the work itself.

The labor clock is being set, in significant part, by where capital has decided to point.

What the Data Doesn’t Yet Tell Us

The bifurcation is visible. The value capture gap is consistent with historical patterns. What the current data can’t yet tell us is whether this is a transitional phase, a steep but temporary adjustment, or a structural reset in the relationship between labor productivity and labor compensation.

Previous automation waves eventually generated new categories of work that reabsorbed displaced labor at higher productivity levels. Factory automation eliminated manufacturing jobs and eventually created the knowledge economy. Whether AI generates a comparable new tier is a genuinely open question. The honest answer is that the data doesn’t resolve it yet.

What isn’t open is whether the disruption is real right now, while the resolution remains uncertain. It is. The workers experiencing the bifurcation today aren’t experiencing a future scenario. They’re in one.

There’s a second layer underneath the bifurcation that the current employment data doesn’t make legible. It moves on a longer timeline, will be harder to see until it has already compounded, and will be significantly more difficult to address once it becomes visible. That’s where Part 2 goes.

Part 2: The Workers Who Were Never Hired. The structural problem underneath the bifurcation, and why it matters more than the displacement headlines.

2 responses to “Who Gets Paid When the Machine Does the Work?”

[…] is Part 2 of a two-part piece on the labor restructuring underway in the AI economy. Part 1 covered the bifurcation already visible in current data and the historical pattern of who captures […]

LikeLike

[…] Workers Who Were Never Hired Who Gets Paid When the Machine Does the Work? Front-Loaded: The Economic Cost of AI’s Capital Concentration AI’s running in four […]

LikeLike